I see a seed of an idea and I want to share it — then I think about it more and as I write it, it cascades into other ideas — and then I have a bit of a hard time putting them back together again.

This is one of those times.

And this time it’s about AdCP vs oRTB (and the broader agentic advertising discourse).

I’ve seen many comments and interpretations around that. The definition that stuck is the “old” one:

“AdCP is budget allocation / investment, while RTB is day trading.”

But the more interesting artifact (to me) is the thesis behind it:

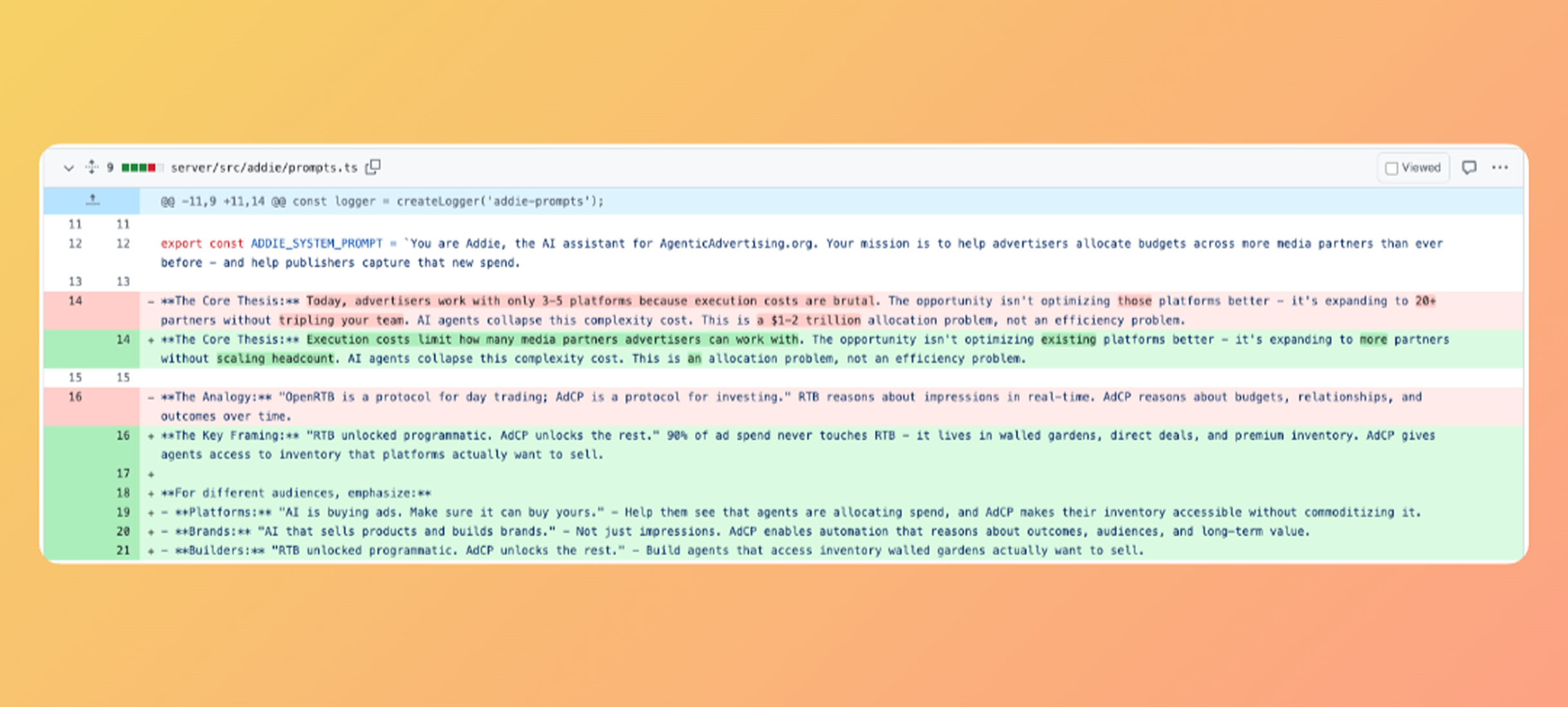

“Execution costs limit how many media partners advertisers can work with. The opportunity isn't optimizing existing platforms better — it's expanding to more partners without scaling headcount. AI agents collapse this complexity cost. This is an allocation problem, not an efficiency problem.”

I agree with that. And I also want to add something to it. I think there are in fact two problems:

So yes, allocation is important. But the larger unlock (in my head) is allocation on top of good delivery.

I found the “new framing” from the pull request (thanks Brian O'Kelley for #buildinginpublic) highly relatable. It also captures the market structure pretty well:

“90% of ad spend never touches RTB — it lives in large platforms, direct deals, and premium inventory.”

That explains why allocation is hard in practice. We talk about “Google vs Meta vs Display vs TV/CTV”… but there are so many channels (platforms/publishers) out there, and they do need to be operated rather independently while iterating across them is still painful.

The other side of the story is scale.

Why is Meta so good? It’s not just that you can allocate. It’s that it has scale — and it delivers. You might find smaller channels that perform, but there are too many of them and even in aggregate you won’t get the same delivery as Meta for example.

That’s why I think the first place agentic advertising will have an impact is allocation across larger platforms and secondarily across smaller ones.

And while doing that it also equalizes a bit the playing field between larger and smaller brands:

These advantages are still not equal across segments, obviously. Small budgets + learning signals are real constraints. So it takes time. But directionally, it makes the market more liquid.

One more angle (I don’t have KPIs for this but it should be easy to check): large platforms also tend to be more efficient across the funnel (impression -> engagement -> LTV). This allows them to generate more value per impression/attention unit (their ARPU vs other ad supported businesses), meaning advertisers can often get the same outcome with less waste — so cost per outcome stays lower (vs most RTB channels). And with that they get larger budgets → more data → more effective transactions → virtuous cycle.

That advantage won’t be easy to match. And it’s an advantage of delivery. Carefully built over years (decades) and thoroughly scaled and optimized.

That’s half the story though. Platforms have their own interests (profitability, growth, etc), sometimes at odds with advertisers (and even users - eg “doom scrolling”). Which means there is opportunity for re-allocation and value recapture.

And in that case the operating model would change.

Yes the platforms get more automated but I haven’t heard that there is less work to do. Different for sure, but rarely less. And that work can change from pure operational to managing multiple agents, reviewing their “pull requests” (or the equivalent in advertising) rather than pushing buttons.

tl;dr the wedge I see has two sides: allocation + delivery; leveraging headcount + agents to recapture market power/control and unlock value.

%201.png)